Business Loans for E-Commerce and Online Retailers in the UK

This article is part of our guide to e-commerce funding.

Edited by the Juice editorial team. Last updated: July 2026.

E-Commerce Funding Challenges in the UK

Running a successful e-commerce business in the UK goes beyond having a popular product or being on Shopify. Growth relies on access to funding, and on funding that bends to the way you actually trade.

Cash flow for online retailers never follows a straight path. Spending on inventory comes months before you see profit. You pay for marketing and then wait weeks for returns to show up. Payouts from sales channels like Amazon and Stripe rarely match the moments when your invoices come due.

Traditional business loans struggle with this cycle. Taking a lump sum and repaying it over several years does not match the shape of retail, and once you are locked into a long-term loan you lose the ability to adjust as the business changes. That can cap growth and add stress.

E-commerce funding is different. Modern options like working capital loans and revolving credit facilities are built to move with your trading cycle, so you can match funding to sales rather than fight the calendar. We cover this shift in more detail in our guide to switching from a business loan to revolving credit.

Where Traditional Loans Fall Short

- Speed. Banks often take weeks to decide, and in e-commerce even a short wait can mean missing a critical buying window.

- What gets reviewed. Banks focus mainly on tax returns and old accounts, while lenders built for e-commerce look at sales data and current performance.

- Flexibility. Repaying a fixed loan monthly does not fit the short inventory or sales cycles that e-commerce runs on.

Your Funding Options in the UK: A Practical Overview

When you start searching for business loans, you will come across a few different options, and each one solves a slightly different problem.

Working Capital Loans UK

Working capital loans give you funding to run daily operations. Unlike property loans or equipment leases, these handle short-term needs and fill the gap between paying suppliers and getting paid by customers. For a deeper walkthrough, see our working capital loans UK guide.

E-commerce businesses often use a working capital loan for:

- Buying inventory ahead of busy seasons

- Paying for marketing campaigns that drive sales

- Covering operating expenses such as rent, delivery, or payroll

Revolving Credit Facility

A revolving credit facility works as a line of credit. You receive approval for a set amount, then you draw funds as you need them, repay, and draw again. Interest is paid only on what you use, not on the full facility. It is closer to a business overdraft or credit card, but built for larger needs. Juice Flex is a continuous line of credit that works alongside your business. An online retailer can draw against an approved line ahead of an inventory order or a paid-ads push, then repay as Amazon, Stripe, or Shopify payouts arrive, with interest charged only on the days a balance sits outstanding.

This type of facility works well for regular inventory purchases, repeated marketing cycles, or situations where funding arrives at different times each month.

Merchant Cash Advance

A merchant cash advance gives you funding up front in exchange for a share of your daily card sales. Repayment happens automatically as a fixed percentage, so you pay more when sales are up and less when sales slow down.

These advances offer speed and flexibility but can be expensive, and the true cost can be difficult to compare with a loan. Always ask for the total figure you will repay before agreeing, and read our guide to MCA factor rates and the true cost of a merchant cash advance before signing. If you are weighing an MCA against a flexible line, we compare the two in MCA vs revolving credit: which ends up cheaper.

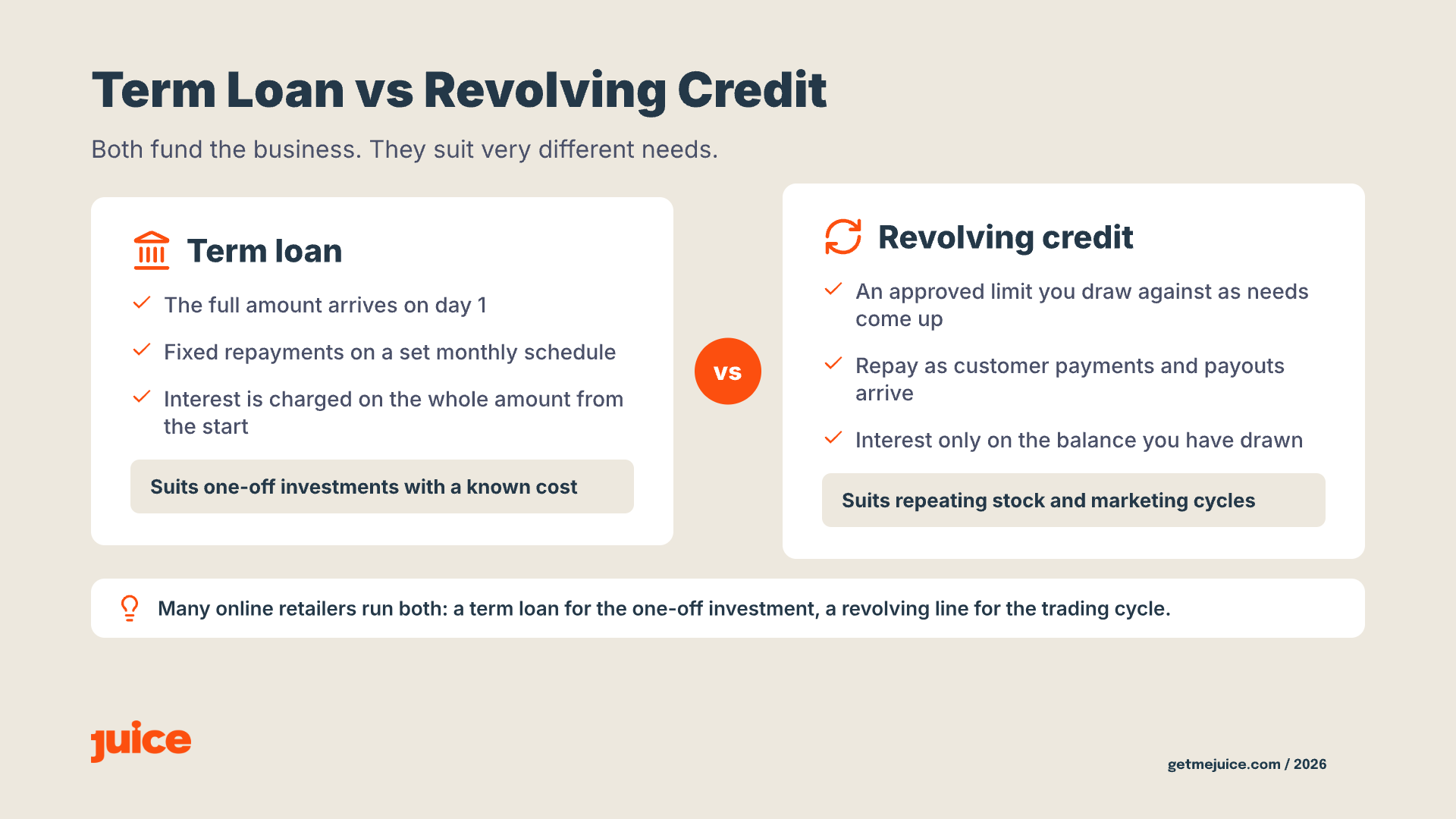

Term Loans and Revolving Facilities: Key Differences

Both term loans and revolving facilities can address funding needs, but they suit different purposes. Term loans provide funding up front with a set repayment plan, which is useful for one-off investments where the cost is clear and predictable. Revolving credit facilities work for ongoing business needs, because they let you use and repay funds as your funding cycle changes, which fits e-commerce trading cycles.

Fast Business Loans: What to Check

Opportunities often come up quickly. A supplier may offer a short-term discount, or you spot a best-seller trending on Instagram. Fast business loans look attractive in those moments, but moving quickly can hide the true cost.

Instead of chasing speed at any cost, look for:

- Pricing that is clear and easy to understand

- No extra or hidden charges, including charges for repaying early

- Lenders who review your current business data and put forward a funding offer you can rely on

Decision times vary by lender. Modern e-commerce-aware lenders often issue decisions within a couple of working days, subject to status, but actual timing depends on the completeness of your application, eligibility checks, and underwriting. Final terms are confirmed in writing before you draw funds.

Business Loan Requirements UK: What You Need

Modern lenders ask for more than just your accounts. The most common requirements are:

- Trading history of at least 6 to 12 months

- Regular monthly revenue that shows your funding can be supported

- A connection to your sales platform and accounting software for a live view of the business

- Registration as a UK limited company with directors based in the UK

You get the fastest decisions when your accounts are up to date and your digital connections are already set up.

Debt Financing Cost: Action Steps

Cost is the first thing to check before accepting any business loan, especially as margins in e-commerce can be tight.

- Always compare total repayment, not just interest rates or APR

- Ask for the exact cost to borrow for the period you actually need

- As an illustrative example, if you borrow £10,000 and repay £11,000 over 6 months, your cost of borrowing is £1,000

- Make sure the extra profit your new inventory generates covers that cost

A clear total-repayment figure, set out in writing before you draw funds, is the single most useful number to ask any lender for.

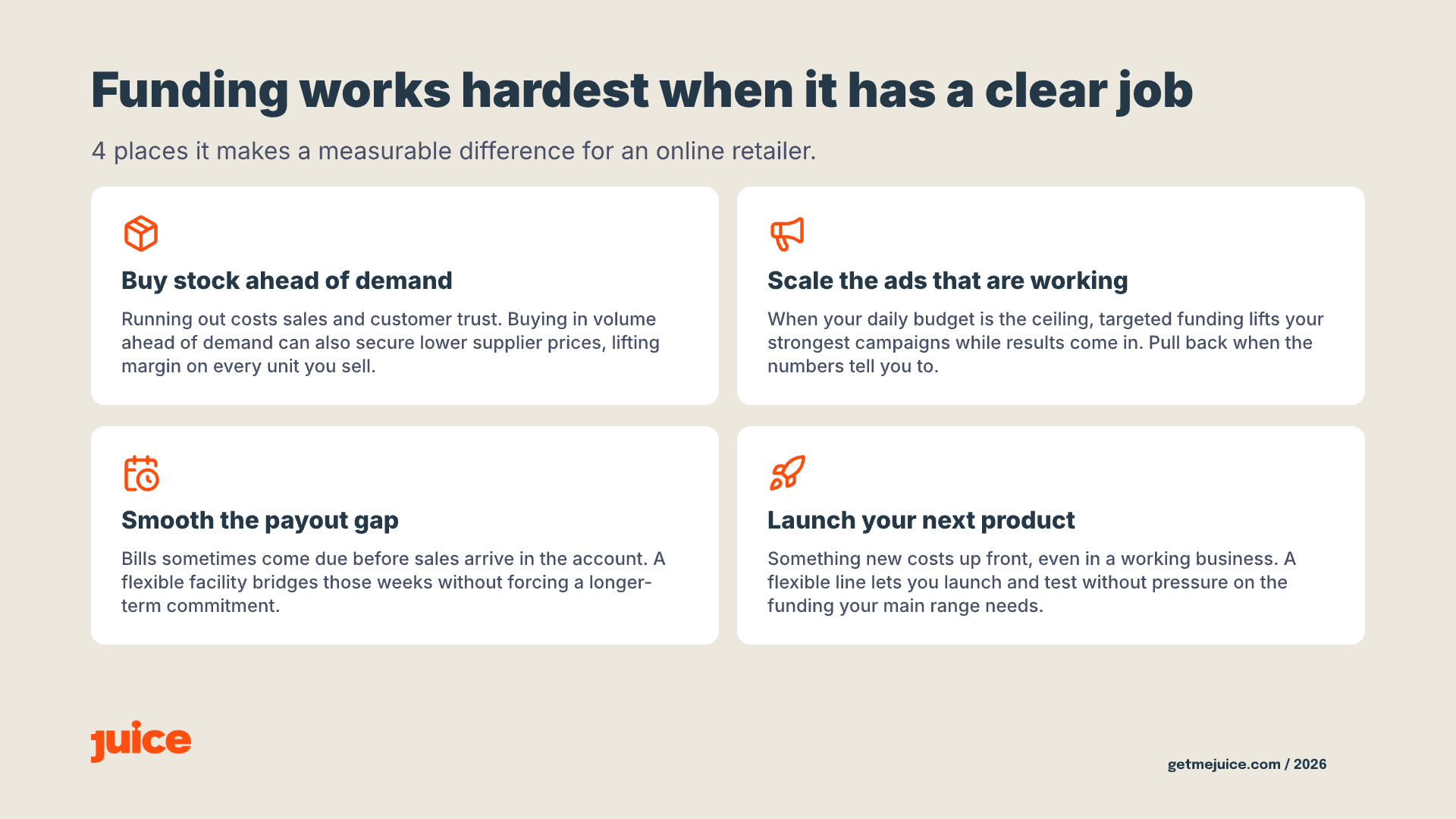

When to Use E-Commerce Funding

Funding is most effective when you target it at a clear goal. Here is where it can make a measurable difference.

Inventory Management

Running out of stock costs you sales and customer trust. Funding to buy in volume ahead of demand can also help you secure lower prices from suppliers, which lifts margin on every unit you sell.

Scaling Marketing Campaigns

If your ads are working but your daily budget is the ceiling, funding can change the picture. Use targeted funding to lift your strongest campaigns while results are coming in, and pull back when the numbers tell you to.

Managing Funding Gaps

Every founder faces times when bills come due before sales arrive in the account. A flexible facility smooths those gaps without forcing a longer-term commitment.

Product Expansion

Launching something new comes with costs up front, even when you already have a working business. A flexible facility lets you launch and test a new product without putting pressure on the funding you need for your main line.

How to Select the Right Lender

Choosing who funds your business matters as much as choosing the type of funding.

- Check whether they understand e-commerce. Sales data, payout cycles, and platform costs should be familiar territory.

- Confirm there are no restrictions or charges for repaying early.

- Look for lenders who offer business insights alongside funding, so you can act on live sales and marketing data rather than month-old reports.

- Ask to see all costs up front, and walk away from anyone hiding charges or relying on unclear factor rates.

What to Weigh Up

When you compare flexible funding options for an e-commerce business, a few things tend to matter most:

- Cost transparency, so the total repayment figure and any fees are set out in writing before you commit.

- Draw and repayment flexibility, so the facility moves with your trading cycle rather than against it.

- Decision clarity, so you know what data the lender will review and how long the process will take.

Weighing options against these points will help you choose a facility that still fits the business in six months' time.

How a revolving credit facility works in practice

For an online retailer, funding needs rise and fall with the trading cycle, climbing ahead of an inventory order or a seasonal peak and easing once stock sells and payouts arrive. A revolving credit facility works differently from a one-off advance. You apply once, and once the facility is approved it stays in place as an agreed limit you can draw against when you need to, rather than a single lump sum paid out on day one.

Drawing down funds. When you need funding, you request a drawdown against your available limit. Each drawdown is subject to a short affordability check rather than being released automatically, and you draw only the amount you need for that purpose.

How repayment works. You repay the drawn balance over a term of up to 24 months per draw, with interest-only options available to ease pressure on cash flow. Repayment is built to flex with how you trade rather than lock you into one rigid schedule. "No early-repayment penalty" means what it says: if you clear a balance ahead of schedule you stop accruing interest from that point, with no exit fee and no charge for repaying early, so strong cash flow directly lowers what you pay.

How you are charged. Interest is charged only on the balance you have drawn, not on the full facility, so a facility that is unused or only partly drawn costs less than one that is fully drawn. We cannot show a specific interest rate here without a representative example, so the rate is confirmed on your individual offer.

Who it suits, and how big a facility. Facilities run from £50,000 to £1 million, so the same structure supports a first-time borrower opening a smaller line through to a scaling business drawing toward the top of the range. A D2C or marketplace brand can draw against the line to fund stock ahead of a Black Friday or seasonal peak, then repay as customers pay and marketplace payouts arrive. .

Common questions

How does the timing of marketplace and processor payouts affect how much funding an online retailer needs?

Marketplaces and payment processors usually hold sales revenue for a set period before releasing it, and that delay can stretch further around busy trading windows or new-seller reviews. The longer the gap between a sale completing and the payout arriving, the more of your own funds you have to float in the meantime to keep paying suppliers, advertising, and shipping. Retailers selling across several channels often face different payout schedules at once, so the funding needed to bridge those gaps depends as much on payout timing as on total sales volume.

How does buying inventory tie up working capital?

Every unit sitting in a warehouse represents funds you have already paid out and cannot use elsewhere until the stock sells and the payout arrives. Buying in larger volumes to secure better unit prices or to cover a busy season deepens that effect, because more of your working capital is held in stock at once. The funds are released again only as you sell through and payments come in, which is why inventory-heavy retailers often feel a squeeze even while sales look healthy.

How should an online retailer plan a funding facility around Black Friday and the Q4 peak?

Demand in the final quarter tends to concentrate into a few intense weeks, so the stock and marketing spend that supports it has to be committed well in advance, often during the late summer and early autumn lull. Planning works best when you map backwards from the peak: estimate the inventory and advertising you need in place before demand arrives, then line up funding to cover that outlay through to the point customer payments and payouts catch up in the new year. Building in some headroom for reorders on fast-selling lines, and for the slower January period when returns are processed, helps avoid being caught short either side of the peak.

The guide and useful links

This article is part of our guide to e-commerce funding. Other articles in this guide:

- Working Capital Loans UK: From Stockroom to Sales Floor

- The True Cost of a Merchant Cash Advance: Factor Rates Explained

- MCA vs Revolving Credit: Which Ends Up Cheaper

If you'd like to discuss how a revolving credit facility could work for your business, talk to the Juice team.