Working Capital Loans UK: Types, Costs and How to Apply

This article is part of our working capital guide.

Working capital funding keeps your business running when cash flow doesn't match your commitments. Whether you're bridging a gap between supplier payments and customer receipts, stocking up for seasonal demand, or seizing a time-sensitive opportunity, the right working capital solution can mean the difference between growth and stagnation.

This guide explains what working capital loans are, how they work, who they're for, and how to choose the right option for your business.

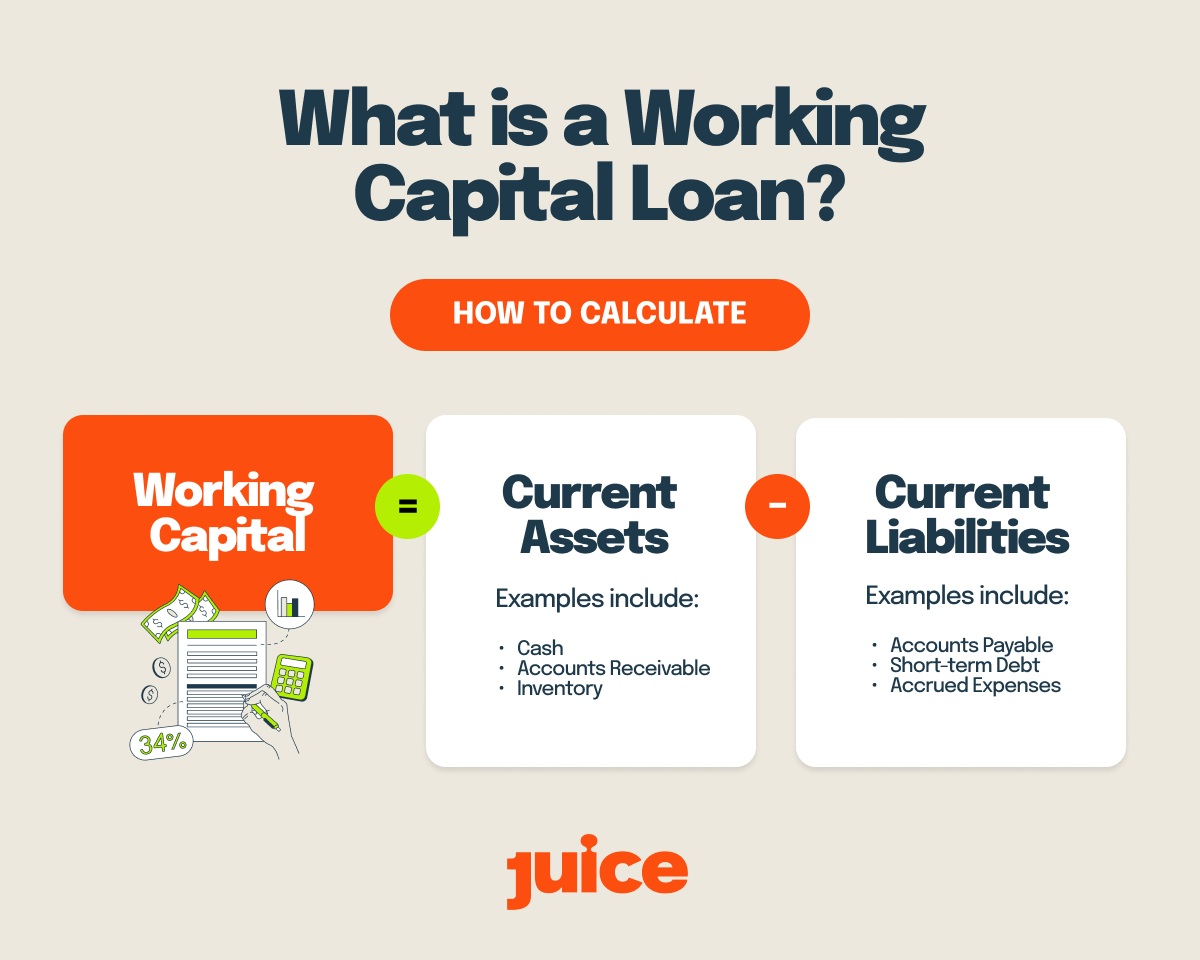

What is a Working Capital Loan?

A working capital loan is finance designed to cover your day-to-day operating expenses rather than long-term investments. It bridges the gap between cash going out (wages, rent, stock, suppliers) and cash coming in (customer payments, sales).

Unlike term loans used for equipment or expansion, working capital funding is flexible and short term, typically running from 3 to 24 months. Rather than buying assets, it keeps your business liquid and your operations moving.

Why UK SMEs Need Working Capital Finance

Most UK SMEs face cash flow timing mismatches:

- You pay suppliers upfront but wait 30, 60, or 90 days for customer payment

- Seasonal businesses need stock before peak trading periods

- Fast-growing companies outpace their cash reserves

- Unexpected costs, such as equipment breakdown or tax bills, disrupt plans

Working capital funding helps you bridge the timing problem between cash going out and cash coming in. It's not a fix for unprofitability; it supports scaling SMEs facing temporary cash constraints. If your business is fundamentally profitable but temporarily cash-constrained, working capital finance is the appropriate tool.

1. Revolving Credit Facilities (RCFs)

A revolving credit facility works like a flexible line of credit with transparent terms. You're approved for a credit limit (£50,000 to £1,000,000), draw down what you need through your dashboard, and only pay interest on what you use. Repay on your terms, and once you've paid back, you can draw again.

Juice Flex is a continuous line of credit that works alongside your business, with fully transparent pricing, no hidden fees, free early repayment, and a decision typically within 24 hours.

Best for: businesses with ongoing or fluctuating cash flow needs who want long-term control and flexibility over their working capital.

For more information, read our complete guide to revolving credit facilities.

2. Business Overdrafts

An overdraft allows you to borrow beyond your bank balance up to an agreed limit. Interest is charged daily on the overdrawn amount. Banks often require security and personal guarantees.

Best for: very small, short-term gaps, though rates can be high and banks can withdraw facilities with little notice.

Read our comparison: RCF vs Business Overdraft — which is right for your business?

3. Short-Term Business Loans

A lump sum borrowed and repaid over 3 to 18 months, usually with fixed instalments. Faster and more flexible than traditional bank term loans, but less flexible than a revolving facility.

Best for: one-off working capital needs with a clear repayment plan, such as funding a single large order.

4. Invoice Finance (Factoring & Discounting)

Invoice finance advances cash against unpaid invoices, typically 80 to 90% of the invoice value upfront, with the balance (minus fees) paid once your customer settles.

Best for: B2B businesses with long payment terms; useful if poor cash flow is specifically due to slow-paying customers.

5. Merchant Cash Advances (Revenue-Based Finance)

A merchant cash advance or revenue-based finance provides a lump sum repaid through a percentage of daily or weekly sales. Repayments flex with revenue.

Best for: retailers and hospitality businesses with daily card transactions; predictable but can be expensive.

Secured vs Unsecured Working Capital Options

It's worth noting that when seeking working capital funding in the UK, you'll encounter 2 main structures:

- Unsecured loans: these don't require physical assets (like property) as collateral. They're usually faster to arrange, and most lenders ask for a personal guarantee in place of asset security.

- Secured loans: these are backed by assets. While they often offer lower interest rates and higher borrowing limits, the application process is longer, and your assets are at risk if you default.

Juice keeps security right-sized to the facility: there's no corporate debenture on facilities under £150,000, so onboarding stays fast without lengthy asset valuations.

Comparison Table: Working Capital Options

When Should You Use Working Capital Finance?

Working capital funding works best when you have a temporary cash flow gap, not a profitability problem. If your business is fundamentally profitable but temporarily cash-constrained, working capital is the right tool. If you're consistently unprofitable, fix the business model first, because borrowing won't solve that.

✅ Good Reasons to Use Working Capital Finance

Bridging payment timing gaps. You've invoiced £100k but won't be paid for 60 days. Meanwhile, suppliers need paying this week.

Seasonal stock purchases. Retailers and e-commerce businesses need to buy inventory 2 to 3 months before peak season (Christmas, summer, back-to-school).

Growth-related working capital strain. Revenue is up 40% year-on-year, but your cash reserves haven't kept pace. You need working capital to fund the lag between buying stock and getting paid.

Unexpected short-term costs. Equipment breaks, tax bills arrive, or a key supplier asks for upfront payment on a large order.

Seizing time-sensitive opportunities. A supplier offers a bulk discount, or a new contract requires immediate stock investment.

Discover the 5 key signs your business needs working capital funding.

❌ When Working Capital Finance Is Not the Answer

Covering ongoing losses. If you're consistently unprofitable, borrowing will only delay the inevitable. Fix the business model first.

Long-term investments. Buying property, vehicles, or major equipment should be funded with term loans or asset finance, not working capital facilities.

Paying off existing debt. Refinancing or consolidation loans may be more appropriate than working capital facilities for managing existing obligations.

How Much Working Capital Do You Need?

Understanding your working capital cycle is the first step in determining how much funding to seek. This cycle represents the number of days your cash is tied up in inventory and accounts receivable before it returns to your bank account as revenue.

The Working Capital Gap Formula

To calculate your gap, you need 3 key metrics from your balance sheet:

- Stock days: how long you hold inventory before it's sold.

- Debtor days: how long it takes your customers to pay you.

- Creditor days: how long you have to pay your suppliers.

Use this formula to identify your working capital requirement:

Working Capital Cycle = (Stock Days + Debtor Days) − Creditor Days

A practical example: you hold stock for 45 days, your customers pay you 60 days after the sale, and you must pay your suppliers within 30 days. The result: (45 + 60) − 30 = 75 days.

This means for every sale you make, your cash is tied up for 75 days. If your monthly operating costs (rent, wages, materials) are £50,000, your business requires approximately £125,000 in working capital just to maintain current operations.

Every business is different, so treat these figures as a starting point and speak to your accountant before committing to a facility size.

Why Your Working Capital Gap Grows as You Scale

A common trap for UK SMEs is overtrading. When your revenue grows by 20%, your working capital gap usually grows by at least 20%. If you don't have the reserves to fund this growth gap, your business can face a liquidity crisis despite being profitable. This is where a revolving credit facility becomes an essential tool to maintain momentum.

Working Capital Loans by Industry

Different sectors have different working capital patterns:

Seasonal Businesses (Hospitality, Tourism, Events)

Challenge: High revenue in peak months, but fixed costs year-round. Need to fund operations during off-season.

Solution: Flexible facilities that can be drawn in low season and repaid during peak trading.

Professional Services & Agencies

Challenge: Long project payment terms (30–90 days) but payroll and contractor costs due immediately.

Solution: Invoice finance or revolving credit to smooth cash flow timing.

Construction & Manufacturing

Challenge: Large upfront material costs before customer payments; project-based cash flow.

Solution: Invoice finance, trade credit, or revolving facilities tied to project milestones.

How to Qualify for Working Capital Finance

Lenders assess your ability to repay from operating cash flow, not asset values. Key criteria:

What Lenders Look For

Trading history. Most lenders want 6 to 12 months of trading, though some specialist providers fund earlier-stage businesses.

Revenue consistency. Lenders prefer predictable revenue. If yours is highly seasonal, you'll need to show you understand your cycle and can repay in peak months.

Affordability. Can you service repayments from forecast cash flow? Lenders typically want to see a debt service coverage ratio (DSCR) of 1.25x or higher, meaning your cash flow covers repayments with 25% to spare.

Credit history. Personal and business credit is checked, but alternative lenders like Juice often take a broader view than banks if your credit isn't perfect.

No significant arrears or CCJs. Active county court judgements or HMRC arrears are red flags. Clear these before applying if possible.

Documents You'll Need

- 6 to 12 months of business bank statements

- Management accounts or recent financials

- Forecast cash flow (for larger facilities)

- Details of existing debt or facilities

- Company directors' details and ID

Approval timelines: bank working capital loans can take 4 to 12 weeks. Alternative lenders such as Juice often return a decision within 24 hours, with funds available within days of approval.

Working Capital Loans with Bad Credit

Many UK business owners worry that a less-than-perfect credit score prevents them from accessing working capital finance. While high-street banks often have rigid "computer says no" policies, alternative lenders take a more holistic view.

If your business is fundamentally profitable but has faced historical challenges, you can still access funding. Lenders will focus more on your current cash flow, recent bank statements, and the strength of your invoices rather than just a legacy credit score.

Working Capital Loan Costs & Pricing

Pricing depends on amount, term, risk, and lender type. The ranges below are illustrative of the UK market rather than quotes from any individual lender, and pricing always depends on your business profile.

Market Rates (2026)

Typical Pricing Ranges (2026)

Revolving Credit Facilities

- Interest: 8–18% APR

- Arrangement fee: 1–3% of facility limit

- Monthly or quarterly reviews

Short-Term Loans

- Interest: 10–25% APR

- Origination fee: 2–5%

- Fixed monthly repayments

Invoice Finance

- Discount fee: 1–3% of invoice value

- Service fee: 0.5–2% monthly on outstanding balance

Revenue-Based Finance

- Factor rate: 1.1–1.4x (you repay £110–£140 per £100 borrowed)

- Typically works out at 15–35% APR equivalent depending on repayment speed

Hidden Costs to Watch For

- Early repayment penalties — some lenders charge if you repay ahead of schedule

- Non-utilisation fees — charged if you don't draw down a minimum percentage of your facility

- Exit fees — charged when the facility ends or is refinanced

- Broker fees — if going through an intermediary, check who pays the commission

Always ask lenders for the total cost of credit and APR, not just the monthly rate, so you can compare like for like. At Juice, we show you the full picture upfront, with no hidden fees.

Working Capital Finance vs Alternatives

Working Capital Loan vs Business Overdraft

Overdrafts are convenient but expensive, often 15 to 25% APR, and can be withdrawn by the bank with little notice. Revolving credit facilities offer similar flexibility with more certainty, longer commitment periods, and often better rates.

Need more detail? Compare revolving credit facilities and business overdrafts.

Working Capital Loan vs Invoice Finance

Invoice finance is technically not a loan — it's an advance against your sales ledger. If your cash flow problem is specifically slow-paying customers, invoice finance may be cheaper and more appropriate than a loan.

Working capital funding is better if your issue is timing between stock purchase and sale, or if you have diverse cash flow needs beyond just invoices.

Bank Loan vs Alternative Lender

Banks typically offer the lowest rates (5 to 10% APR) but require strong financials and security, and approval can take 4 to 12 weeks. Alternative lenders like Juice often return a decision within 24 hours and take a broader view of credit history, though rates are typically higher than traditional banks.

The trade-off is speed and flexibility against cost.

How to Apply for Working Capital Finance

Step 1: Assess Your Actual Need

Don't borrow more than you need. Calculate your working capital gap, forecast your cash flow, and determine:

- How much you need

- When you need it

- When you can realistically repay

Step 2: Choose the Right Product

Match your need to the right structure:

- Fluctuating needs? → Revolving credit facility

- One-off purchase? → Short-term loan

- Slow-paying invoices? → Invoice finance

- Card-based revenue? → Revenue-based finance

Step 3: Compare Lenders

Get quotes from at least 3 providers. Compare:

- Total cost (APR and fees)

- Speed of decision and funding

- Flexibility (early repayment, drawdown terms)

- Ongoing relationship and support

Step 4: Prepare Your Application

Gather bank statements, financials, and a simple cash flow forecast. Be ready to explain:

- Why you need the funding

- How you'll use it

- How you'll repay it

Step 5: Apply and Review Terms

Once you have an offer, read the facility agreement carefully before signing. Check:

- Interest rate and fees

- Repayment terms and schedule

- Covenants or restrictions (e.g. minimum cash balance, debt limits)

- What happens if you miss a payment

Managing Working Capital Effectively

Borrowing is one tool. Managing working capital proactively reduces how much you need to borrow:

1. Speed Up Customer Payments

- Offer early payment discounts (e.g. 2% off if paid in 10 days)

- Invoice immediately after delivery

- Follow up on overdue invoices promptly

- Use direct debit or card payments where possible

2. Negotiate Better Supplier Terms

- Ask for 30 or 60-day payment terms instead of immediate payment

- Build strong relationships with key suppliers for flexibility during tight periods

3. Optimise Stock Levels

- Don't over-order; use just-in-time principles where practical

- Identify slow-moving stock and discount it to free up cash

- Use demand forecasting to match stock to actual sales patterns

4. Forecast Cash Flow Monthly

- Build a rolling 13-week cash flow forecast

- Identify pinch points in advance

- Arrange funding before you're in crisis, because lenders prefer to fund healthy businesses rather than rescue struggling ones

For more information, check out our article: How to Manage Cashflow Gaps Without Breaking the Bank (verify live slug before publish — this link 404'd in the 12 June review)

Frequently Asked Questions

What's the difference between working capital and cash flow?

Cash flow is the movement of money in and out of your business. Working capital is the net difference between your current assets (cash, stock, receivables) and current liabilities (payables, short-term debt). Positive working capital means you can meet short-term obligations.

Can startups get working capital loans?

Most lenders require 6 to 12 months of trading history. Pre-revenue startups typically need equity investment, founder loans, or grants rather than working capital debt.

Do I need to provide security or a personal guarantee?

It depends on the lender and the facility size. Banks usually require both security and personal guarantees. Juice right-sizes security to the facility: there's no corporate debenture for facilities under £150,000, and facilities under that threshold are instead supported by a personal guarantee, while facilities of £150,000 and above are secured by a corporate debenture.

How quickly can I get working capital funding?

With an alternative lender such as Juice you could have a decision within 24 hours, depending on complexity and due diligence. A traditional bank can take 4 to 12 weeks.

What if I'm refused by my bank?

Alternative lenders, specialist finance providers, and fintech platforms often lend to businesses that banks decline, particularly if you're early-stage, fast-growing, or have imperfect credit.

Can I have multiple working capital facilities?

Yes, but lenders will want to know about existing commitments. Multiple facilities can be useful (e.g. an overdraft for day-to-day and a revolving facility for seasonal stock), but manage them carefully to avoid over-leverage.

Next Steps: Get the Right Working Capital Solution

Working capital finance isn't one-size-fits-all. The right option depends on your industry, cash flow cycle, growth rate, and how you plan to use and repay the funds.

If you need flexible, ongoing access to working capital, a revolving credit facility may be the best fit. If you have a one-off need with a clear repayment plan, a short-term loan could be more appropriate. If slow-paying invoices are the issue, invoice finance might be the answer.

Get Smart Growth Capital™ for your business. At Juice, we help UK business owners see their profitability, plan their growth, and fund their momentum with transparent, flexible funding.

Why businesses choose Juice Flex:

- Revolving credit facilities from £50k to £1M

- Decision in 24 hours, with funds available within days of approval

- Transparent pricing, no hidden fees

- Repay early anytime, no penalties

- No corporate debenture on facilities under £150k

Juice lends to UK limited companies and LLPs with £20k+ monthly revenue. Subject to status and lending criteria.

See how much you qualify for. Apply now to get your customised offer. Checking eligibility won't affect your credit score. Calculate Your Working Capital →

Related Guides: